Q3 2024: Are prices set to stabilise at the end of 2024?

Here are the main observations that can be made at the end of the third quarter of 2024, taking into account current data on the property and rental market. This quarter was marked by a number of significant trends, both in terms of prices and financing conditions, which directly influence the behaviour of market players.

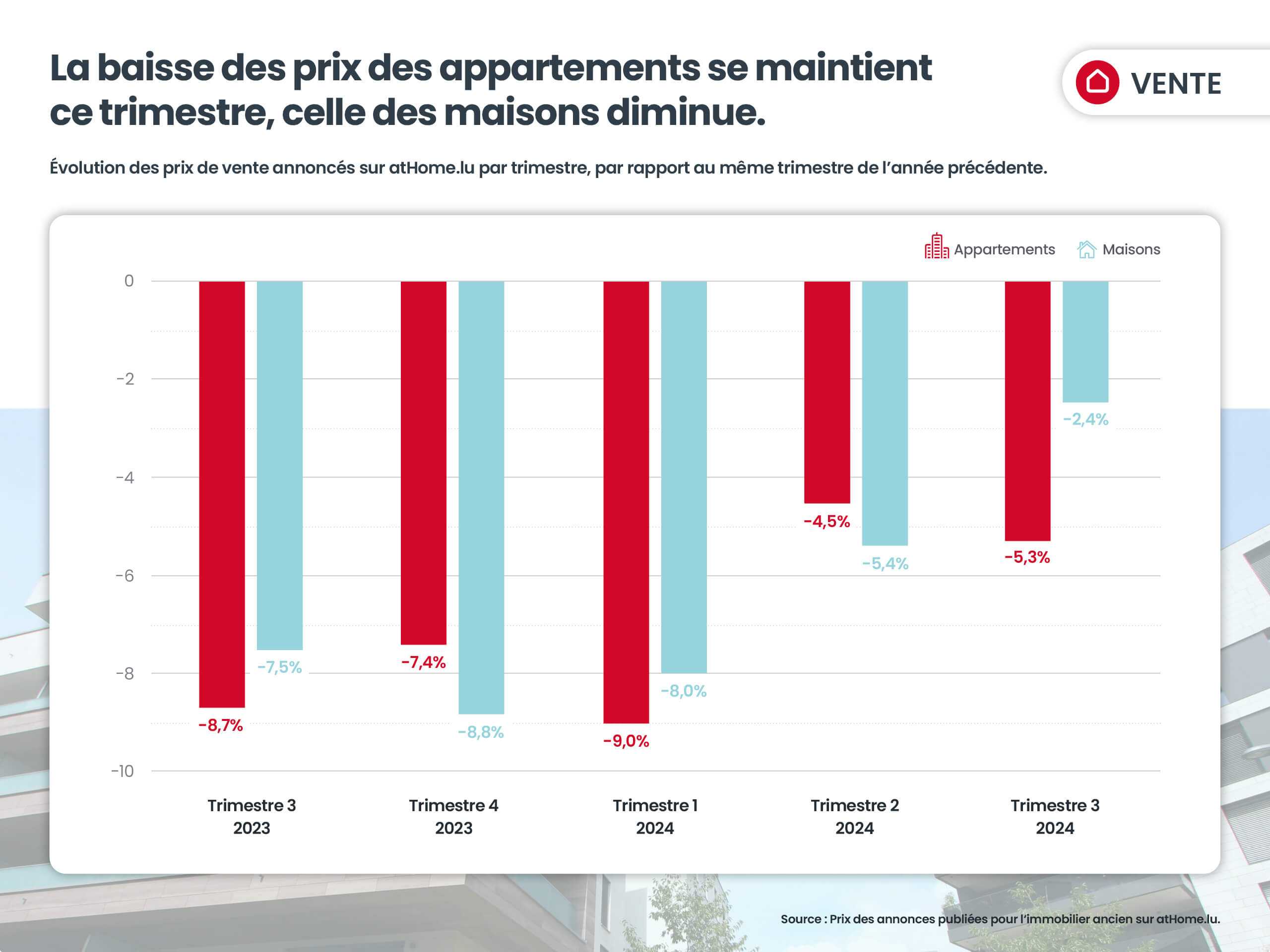

- Announced sales prices which are still down on 2023, but are tending to stabilise compared with previous quarters - for both houses and flats.

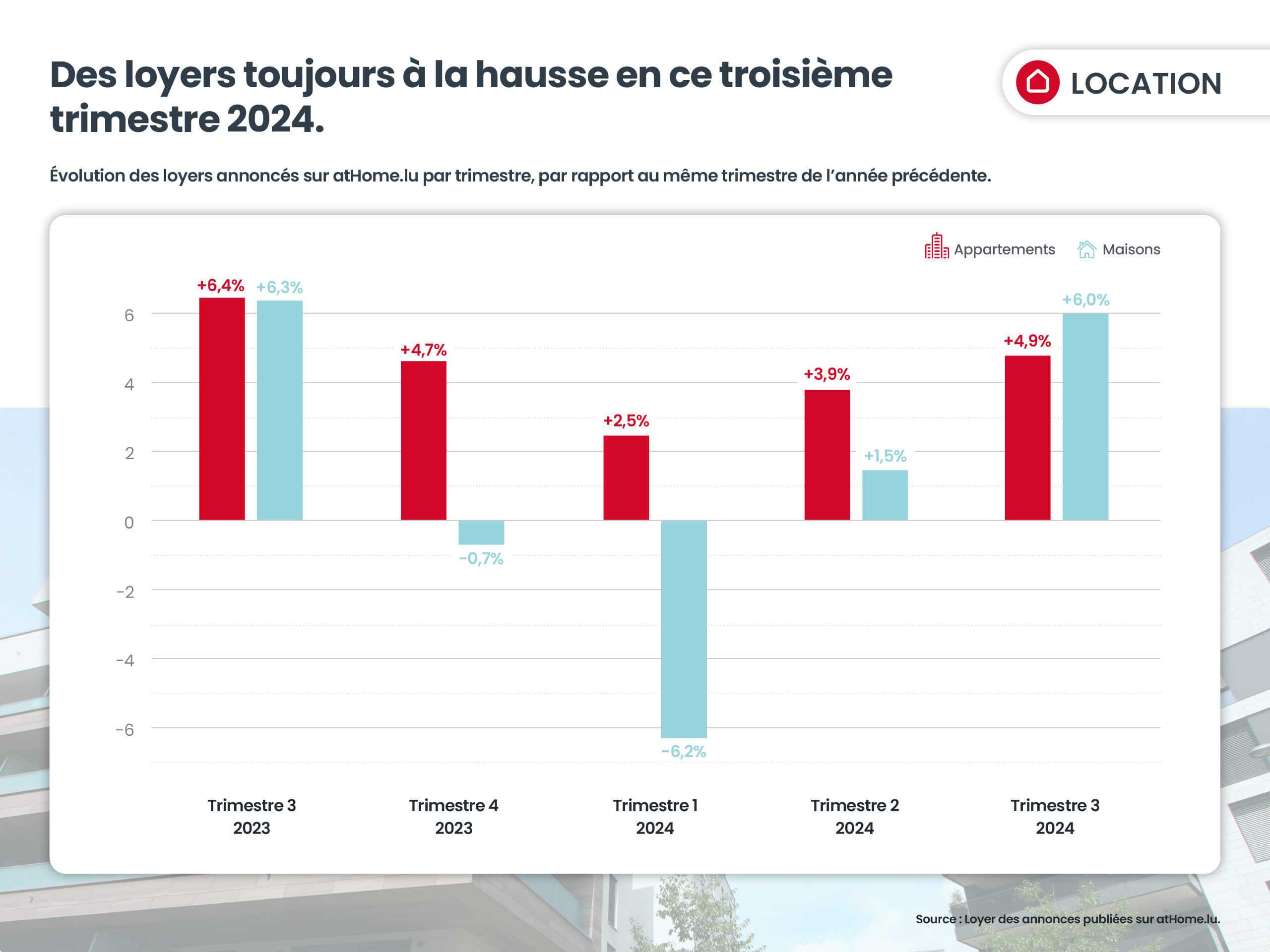

- Rents which continue to rise quarter on quarter, particularly for houses.

- Lower interest rates on home loansThis follows two successive cuts since June (25 basis points) in key rates by the European Central Bank (ECB), and a 50 basis point cut in September by the US Federal Reserve (FED).

In other words, rents are continuing to rise, while house and flat selling prices are showing signs of stabilising. At the same time, interest rates are falling sharply, making it easier to borrow, invest and buy. This combination of stabilising prices and advantageous financing conditions, if it continues over the coming months, could attract many potential buyers to the market.

Sales prices: a slowdown in the downward trend

A comparison of advertised sales prices in the third quarter of 2024 with the same quarter of the previous year shows that the decline is continuing, but is showing signs of slowing.

The fall in flat prices (-5,3%) is fairly comparable to that observed in the second quarter of 2024 (-4,5%), while falling house prices (-2,4%) is well below the declines seen in previous quarters.

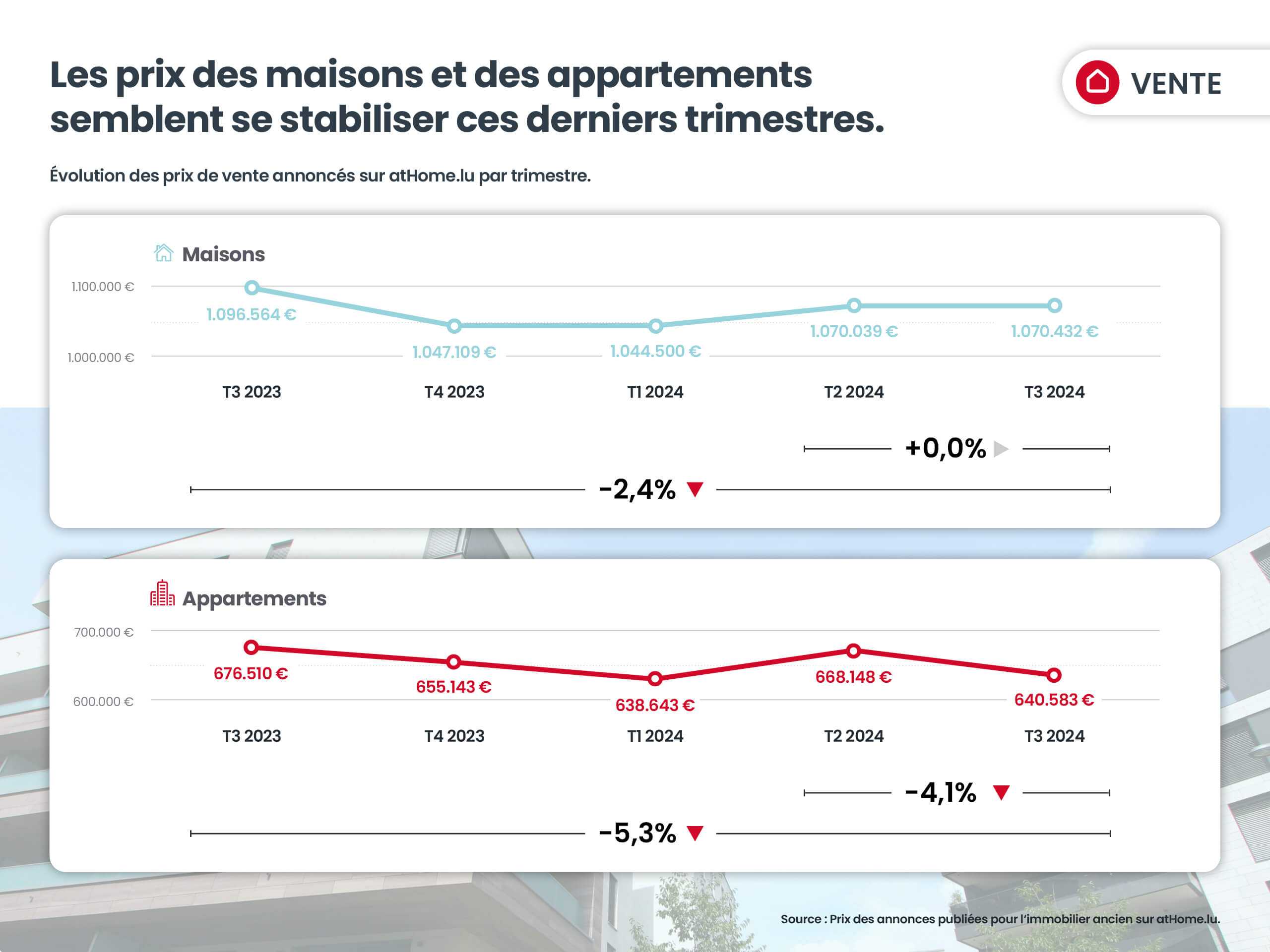

An analysis of price trends over the last few quarters reveals a trend towards stabilisation, following a period of decline in 2023. For houses (+0,0% between T2 and T3 2024) than for flats (-4,1% between Q2 and Q3 2024), third-quarter figures seem to confirm a return to equilibrium over 2024, and even a slight rise in house prices.

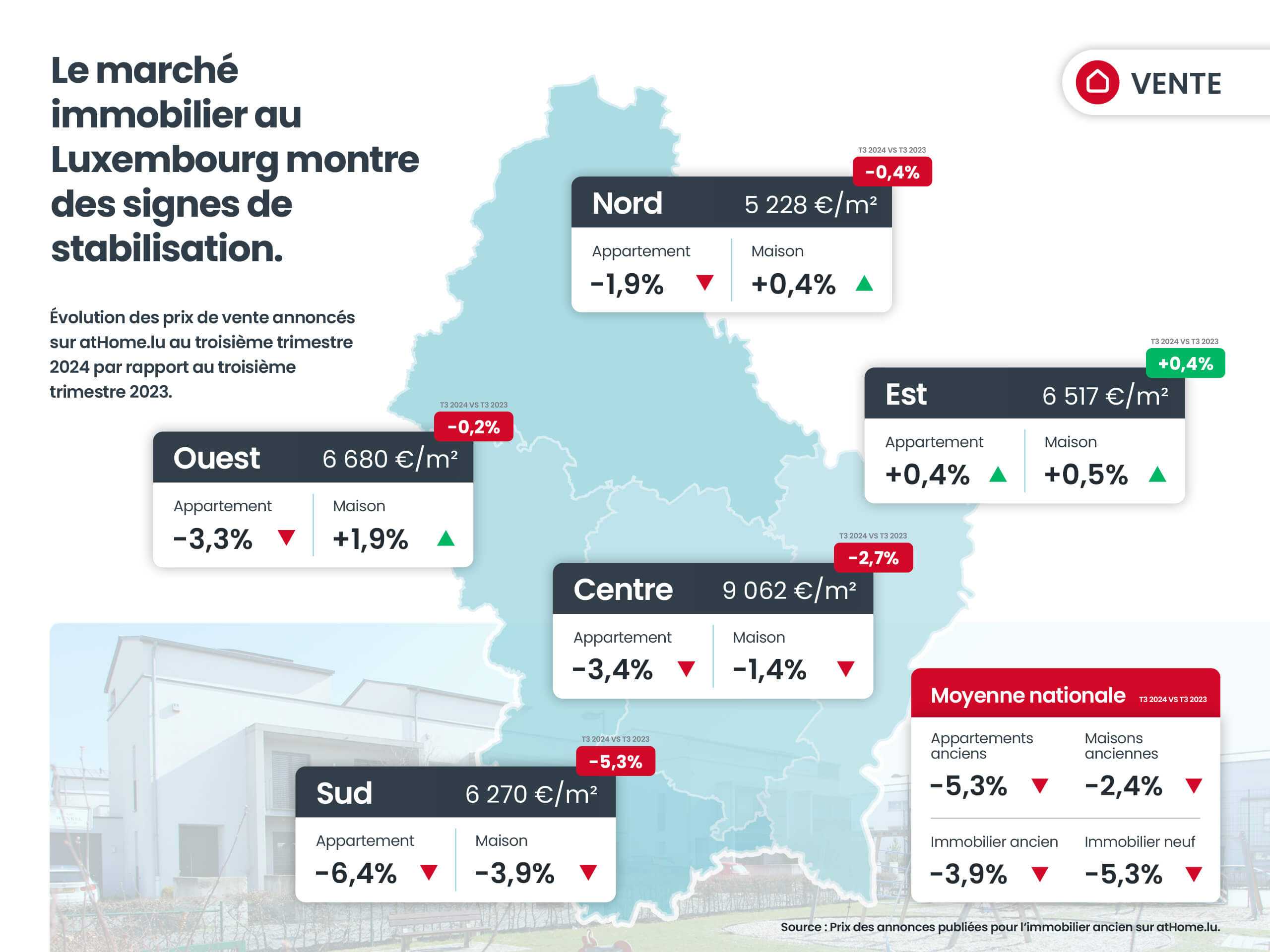

Breakdown of average selling prices and changes by region (Q3 2024 vs. Q3 2023) :

Generally speaking, new property prices (-5,3%) are falling more than those for existing properties (-3,9%).

For existing properties, flat prices (-5,3%) are falling more than those for houses (-2,4%).

Detailed analysis reveals different realities in each region of the country:

- Centre: €9,062/m2where flat prices have fallen from -3,4% and -1,4% for a bearish average of -2,7%.

- North: €5,228/m2with a very slight increase in house prices with +0,4% compared with a fall for flats of -1,9%.

- South: €6,270/m2with an average of -5,3%or -6,4% for flats and -3,9% for homes.

- West : 6 680 €/m2where we are seeing a rise in prices for houses of +1,9% faced with a fall in flat prices of -3,3%.

- East: €6,517/m2which recorded very slight increases in house sale prices +0,5% as well as flats +0,4%.

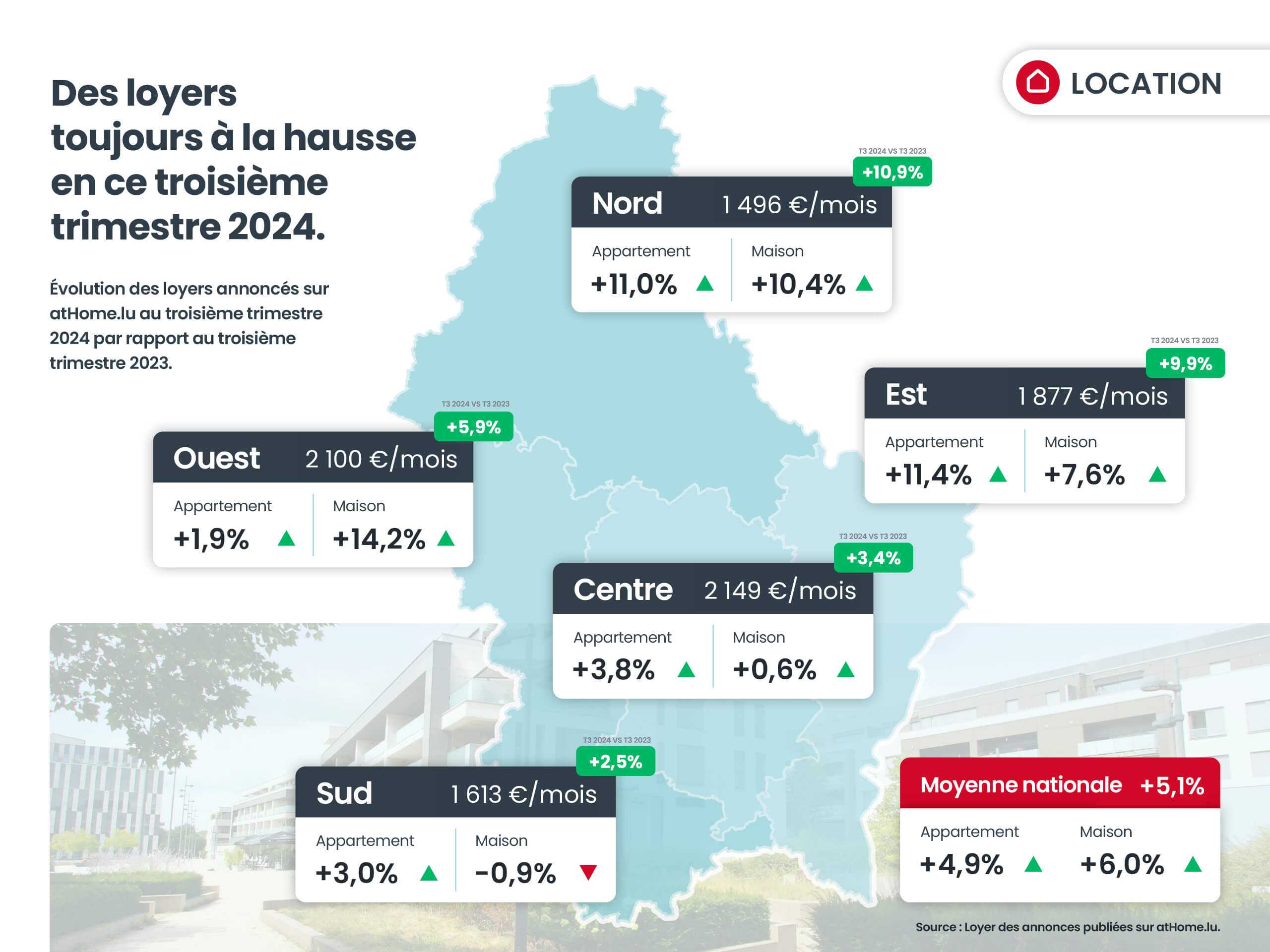

Rental market: rents still on the rise

The rental market continued its upward trend in the third quarter, with an average increase in rents of +5,1% at national level. This increase reflects the dynamic seen throughout the year, fuelled by strong demand and limited supply.

A comparison of advertised rents in the third quarter of 2024 with the same quarter of the previous year shows that the rise continues and even strengthens - particularly for houses. The rise in flat prices (+4,9%) is in line with that seen in the second quarter of 2024, while the rise in house rents (+6,0%) is up significantly on previous quarters.

Breakdown of average rents and their evolution by region Q3 2024 vs Q3 2023:

Detailed analysis shows an upward trend across the country, although the extent of the increases varies widely depending on the type of property and the region.

- Centre: €2,149with a moderate increase in +3,4%. Flats are up +3,8% and houses by +0.6%.

- North: €1,496with the strongest growth at +10,9%. Flat rents increase by +11,0% against +10,4% for homes.

- South: €1,613where there was a slight fall of -0,9% for houses, while rents for flats rose by +3,0%.

- West: €2,100which has seen an explosion in house rents, with an increase of +14,2% against a smaller increase in rents for flats in +1,9%.

- East: €1,877with an overall increase of +9,9%. Rents rose by +11,4% for flats against +7,6% for homes.

What can we expect over the coming months?

Over the next few months, a number of factors suggest that the property market could continue to move towards stabilisation, or even a moderate recovery.

As far as selling prices are concerned, a stabilisation seems to be taking shape, with a moderate upward trend for houses, especially in the West, East and North regions.

Flats, meanwhile, should continue to move towards a situation of price equilibrium, particularly in certain regions where falls are still marked.

At the same time, interest rate cuts by the ECB and the FED will make access to credit more attractive to potential buyers, and could encourage a resumption of borrowing and property investment.

This combination of more moderate prices and favourable financing conditions could stimulate positive momentum, while maintaining pressure on the rental market, where rents should continue to rise, albeit possibly at a more measured pace. The market will remain under pressure, particularly in the most sought-after areas, but price trends should tend towards a degree of stabilisation as economic and financing conditions normalise.

What the experts say

Written by

atHome.lu

Posted on

09 October 2024